What's behind China’s cryptocurrency ban?

来源:World Economic Forum;发表于:2022-02-12;人气指数:408

What's behind China’s

cryptocurrency ban?

https://www.weforum.org/platforms/shaping-the-future-of-financial-and-monetary-systems/articles/what-s-behind-china-s-cryptocurrency-ban

China's cryptocurrency ban came into force in September

2021

Image: REUTERS/Florence Lo/Illustration

31 Jan 2022

Francis Shin

Research Assistant, Europe Center, Atlantic Council

*The People's Bank of China argues that its ban on

cryptocurrencies is to curtail financial crime and prevent economic

instability.

*However, China's cryptocurrency ban comes amid fears

that cryptocurrencies were facilitating capital flight from its markets,

bypassing conventional restrictions.

*China's cryptocurrency ban is part of a new trend in

Chinese economic policy toward greater state intervention, epitomized in the

“common prosperity” campaign.

In late September 2021, the People’s Bank of China

(PBOC) banned all cryptocurrency transactions. The PBOC cited the role of

cryptocurrencies in facilitating financial crime as well as posing a growing

risk to China’s financial system owing to their highly speculative nature.

However, one other possible reason behind the cryptocurrency ban is an attempt

to combat capital flight from China.

According to the Chainalysis Blockchain data platform,

more than $50 billion worth of cryptocurrency left East Asian accounts to areas

outside the region between 2019 and 2020. As China has an outsized presence in

East Asian cryptocurrency exchanges, Chainalysis staff believe that much of

this net outflow of cryptocurrency was actually capital flight from China.

Although Chainalysis does not have a definitive figure for how much capital

fled China between 2019 and 2020, they estimate that it could be as high as $50

billion.

Capital controls and cryptocurrency exchanges

China places an annual limit of $50,000 for the purchase

of foreign currencies as part of its already strict capital controls. As

such, the capital flight facilitated by cryptocurrency is especially notable.

Previously, the rich in China got around capital

controls by purchasing foreign real estate, creative invoicing for

international trade and even coercing their employees to transfer money to

foreign bank accounts. With Bitcoin, residents in China have been able to

acquire foreign assets more easily, free from the scrutiny of Chinese

authorities. Given the decentralized nature of Bitcoin and many other

blockchain-based cryptocurrencies, they can be used to circumvent capital

controls far more easily than a conventional currency exchange that

uses the banking system.

Despite the strict capital controls in place, Chinese

authorities have always been wary of capital flight. The effectiveness of these

capital controls is somewhat debatable, as some commentators argue that

capital flight grew significantly between 2009 and 2018. Meanwhile, in

2017, the PBOC banned the operations of cryptocurrency exchanges within

China. (The 2017 ban did not go so far as to forbid the ownership or mining of

cryptocurrency, which the 2021 ban finally prohibits.) Although China did not

cite capital flight as a reason for its cryptocurrency restrictions in 2017,

Chinese authorities did place additional restrictions on overseas

investments by Chinese companies that same year. In some ways, the 2017

restrictions on cryptocurrency exchanges in China can be seen as the harbinger

of the subsequent tightening of outward investment of Chinese companies that

year.

Chainalysis also notes that much of the capital flight

out of East Asia is facilitated by the stablecoin, Tether (USDT), a

cryptocurrency notionally pegged to the value of the US dollar (USD).

Tether became more popular in 2017 following the PBOC’s restrictions on crypto

exchanges in China. Trading Bitcoin for Tether was already made illegal by the

PBOC’s 2017 prohibition on cryptocurrency exchanges, but it was still possible

for Chinese cryptocurrency traders to acquire Tether from discreet trade with

over-the-counter brokers or through the use of foreign bank accounts. According

to former Grayscale Director of Research Philip Bonello, Tether is

especially popular in China because its value is stable from being

hypothetically pegged to the US Dollar, making it easier to exchange to the

fiat currency of a user's choice.

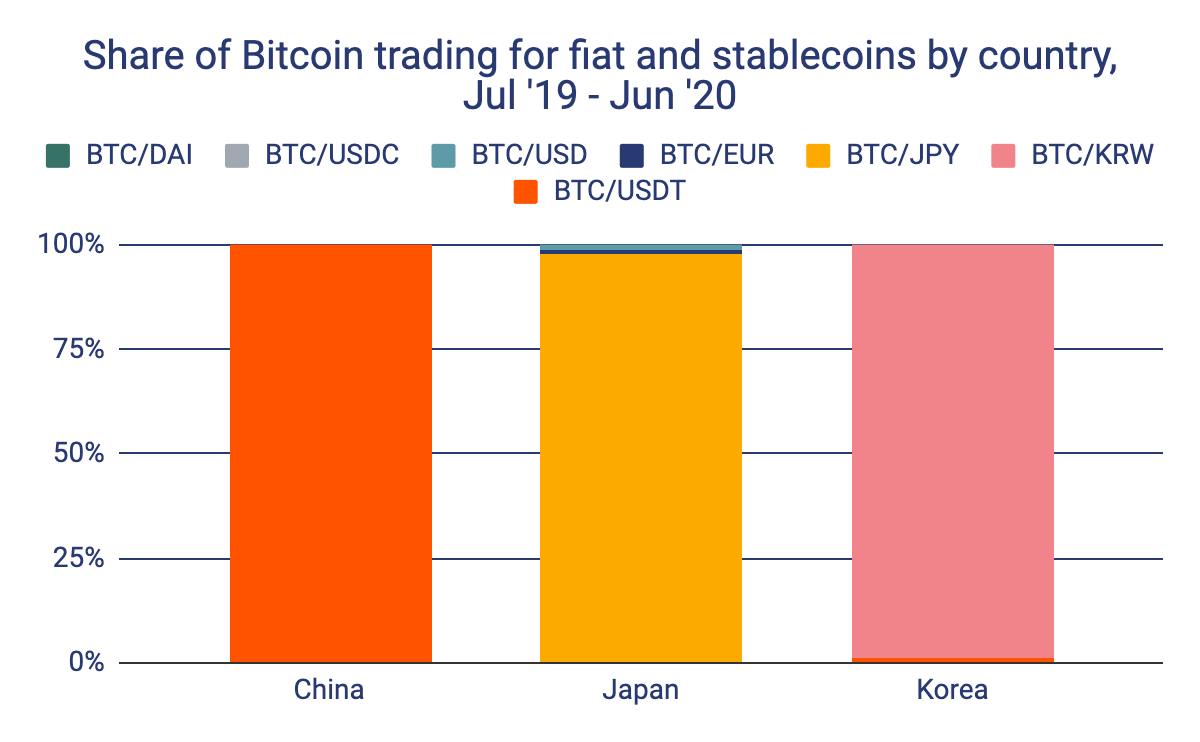

Currencies included: BTC, DAI, USDC, USDT.

Image: Kaiko

Common prosperity and capital controls

The threat of capital flight remains a priority for the

PBOC as the Chinese economy recovers from the COVID-19 pandemic, especially as

China launches its “common prosperity” campaign. Former PBOC advisor Li

Daokui has warned that the relatively fast economic recovery of the

US could fuel greater capital flight, as Chinese residents may be inclined to

purchase assets in the US for greater financial security.

Moreover, the common prosperity drive emphasizes a

heavier statist approach to managing China’s economy, as well as a more

inward-looking economic strategy. Notably, the outlawing of cryptocurrency

transactions happened only a month after the announcement of the common

prosperity programme. This cryptocurrency ban may have also been brought in to

curtail outward investments and instead encourage the rich in China to accept

higher income taxes and to contribute their wealth domestically.

Altogether, there is strong evidence to suggest that the

cryptocurrency prohibition was a response to the perennial problem of capital

flight from China. Given that a huge amount of capital flight already occurred

through cryptocurrency exchanges, the PBOC will have been aware that

cryptocurrency was exacerbating China’s chronic issue of capital flight.

With the common prosperity programme, China aims to curb

capital flight and encourage the domestic circulation of people’s wealth.

China’s attempts at wealth redistribution would be far more difficult to

accomplish if the rich circumvented China’s already strict capital controls

through offshore cryptocurrency exchanges and acquired overseas assets.

Nevertheless, in spite of the political imperative, such a

strict ban on cryptocurrency transactions will be very difficult to

enforce. Capital flight, enabled by cryptocurrency transactions, is likely to

continue. Time will tell how seriously the eventual economic impact will be.